Opportunites

The following area provides thoughts and research on individual equities and trading ideas that AOA are considering or have considered as potential trade or investment opportunities.

This does not constitute investment advice. Please see full Terms and Conditions below.

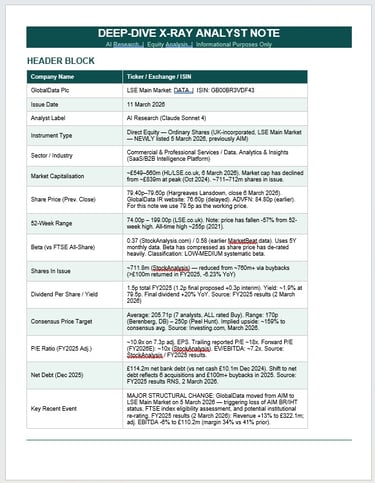

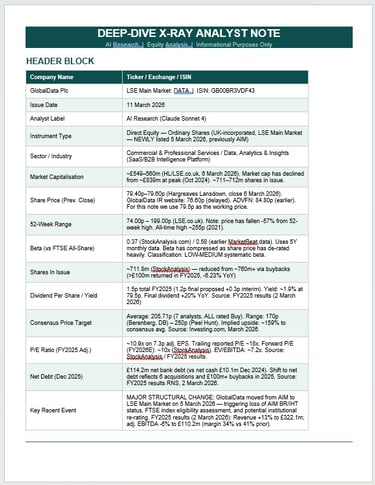

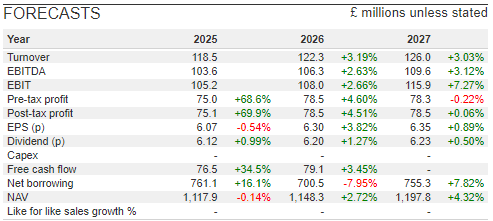

Intertek - Bid potential for 15-20% Upside? - Apr 30th 2026

_________________________________________________________

_________________________________________________________

Filtronic (FTC) - Another big win with SpaceX presents 20-40% upside opportunity! - Aug 26th 2025

AOA does not currently hold FTC

1. RNS Highlights (Last Six Months)

£47.3m ($62.5m) SpaceX Order (26 Aug 2025)

Filtronic secured its largest single order to date for GaN E-band RF modules, with production starting FY2027 and material revenues expected in FY2027–28. Represents a tech leap with GaN offering superior SWaP-C over legacy GaAs products.Option Exercise Update (July 2025)

Issued ~76,816 shares upon option exercise — standard dilution event.Other RNS Activity (14 Nov 2024–Jan 2025)

Includes trading updates, director appointments, design center opening, etc., but no high-impact RNS within the last six months.

2. Business Model & Sector KPIs

Filtronic designs and manufactures RF, microwave, and mm-wave subsystems (GaN, E-band transceivers, amplifiers, diplexers) aimed at space (e.g., Starlink), aerospace, defence, critical comms, telecom infra. Key performance indicators:

Order Backlog & Product Portfolio — SpaceX contract is transformational.

Gross Profit Margins — likely high for RF niche.

Tech Transition Execution — GaN adoption viability.

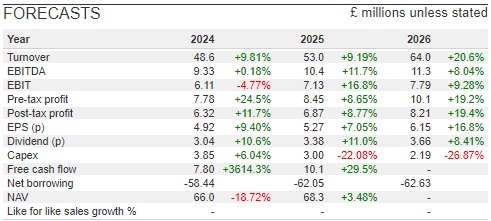

Revenue Growth — grew 121% YoY in 2025 (to £56.3m); net income up 347% YoY to £14.05m.

R&D-to-sales, manufacturing scaling, and margin sustainability.

3. Fundamentals Snapshot

Revenue: £56.3m TTM, up 121% YoY.

Net Income: £14.05m TTM, significant improvement.

Balance Sheet: Appears debt-free at present.

Volatility: High weekly vol (~8%), above market average.

4. Technical & Price Structure

Current Price: ~144 p. Range: 52-week low 61.5 p → high 173 p.

Liquidity: Average daily volume ~1M+ shares; volatility elevated.

Technical setup: Likely range-bound post SpaceX move; potential breakout pending revenue horizon.

5. Sentiment & Analyst Views

Earnings & Growth: Strong TTM performance.

Future Estimates: Earnings growth forecasted to decline 45% per annum over next 3 years — likely reflects phasing of the SpaceX order.

Minimal broader analyst coverage; sentiment largely reactive to RNS events.

6. Valuation Triangulation

P/E: ~22.3× TTM; Forward P/E ~49× (likely reflecting order delivery ramp).

P/S: ~5.3× TTM.

Intrinsic Value (DCF estimate):

SpaceX contract (~£47m+ future revenue) plus existing business suggest fair value ~180–220p, assuming phased revenue from 2027, high margin, and rollout across sectors.Volatility/Execution Premium: Elevated risk justifies premium but cautious multiples.

7. Scenario & Risks

Bull: SpaceX revenue delivered; new GaN wins; scale achieved 220–260p+50–80%

Base: Order holds; moderate scale; margin stable 180–200p +25–40%

Bear: Delivery delays; competitive pressure; backlog slips 120–140p –10 –0%

Key Risks: Execution of GaN production; high concentration (SpaceX dependency); long lead times; capex investment needs; volatile sector dynamics.

8. Catalysts

SpaceX Delivery Progress — production timeline and orders beyond FY2027.

Additional GaN Wins with other satellite or aerospace clients.

FY2025 Results (likely late Autumn 2025) — revenue breakdown, margin commentary, capex guidance.

Market Reaction to Contracts — narrative shift post-order; visible execution metrics.

Investment Memo

Thesis:

Filtronic has secured a landmark £47m GaN E-band order from SpaceX, validating its engineering prowess and offering a material revenue runway from FY2027–28. Revenue and EPS growth have surged YoY, and the balance sheet remains strong. The GaN platform positions Filtronic at the forefront of space and defense RF communications premium layers.

Valuation & Upside:

DCF/light modeling suggests fair value of ~180–220p, assuming production and scale delivery. Present price (~144p) implies +25–55% upside. The P/E multiple is elevated but justified by the prospect of SpaceX revenues and tech premium.

Key Risks:

Delay or non-execution of SpaceX delivery

High concentration in one client

Manufacturing scale or quality issues

Near-term earnings visibility limited

Watch Items:

Production start tracking for GaN modules

FY2025 results for margin, R&D, capex guidance

Additional client wins, technology adoption acceleration

_________________________________________________________

Super Market Income REIT - An opportunity to own part of the UK Supermarket retail space? - Oct 23rd 2024

AOA does not currently hold SUPR

Supermarket Income REIT plc (LSE:SUPR) is dedicated to investing in supermarket property forming a key part of the future model of grocery. Their supermarkets are let to leading supermarket operators in the UK and Europe, diversified by both tenant and geography. They are the largest landlord of omnichannel supermarkets in the UK.

Supermarket Income REIT (LSE: SUPR) reported solid performance for the fiscal year ended June 30, 2024, despite challenges in the broader economic environment. Here’s a detailed analysis of the latest results and a balanced bull and bear case for long-term investment.

Latest Results Overview

For FY24, SUPR achieved a 13% year-over-year increase in net rental income, reaching £107.2 million. This growth was primarily driven by new acquisitions and upward-only rent reviews, which resulted in a 12% increase in annualized passing rent to £113.1 million. Adjusted earnings per share improved by 4.4% to 6.1p, and the portfolio's valuation rose 5% to £1.8 billion. However, EPRA net tangible assets (NTA) per share dropped by 6% to 87p due to valuation adjustments amid a higher interest rate environment. Debt metrics remain manageable, with a stable loan-to-value (LTV) ratio at 37% and recent refinancing activities fixing borrowing costs at an average of 3.8%

Bull Case

Defensive Business Model: SUPR’s focus on omnichannel supermarkets, which serve both in-store and online grocery shoppers, positions it well in a resilient sector. With 100% occupancy rates and long-term, inflation-linked leases primarily with top-tier grocers like Tesco and Sainsbury's, the REIT offers a stable income stream. The growing online grocery market adds to the long-term demand for these properties, supporting income growth.

Accretive Acquisitions: SUPR has continued to grow its portfolio with strategic acquisitions. In FY24, it expanded its footprint with 20 new assets in the UK and France, including a portfolio of Carrefour stores. These acquisitions were executed at attractive yields, enhancing earnings and diversifying geographic exposure, which could mitigate risks associated with the UK market

Attractive Dividend Yield: The REIT offers a fully covered dividend, with the FY24 payout at 6.1p per share, a slight increase from the previous year. The target for FY25 has been set at 6.12p. Given the defensive nature of grocery retail and SUPR’s secure income base, the dividend provides a steady cash return in a volatile market.

Potential Interest Rate Tailwinds: SUPR has been cautious with leverage, maintaining a moderate LTV. As expectations for rate stabilization or potential cuts emerge, this could benefit real estate valuations and lower refinancing costs, potentially boosting the stock's appeal

Bear Case

Valuation Pressure Due to Interest Rates: The decrease in EPRA NTA per share reflects challenges in the real estate market due to higher borrowing costs. If rates remain elevated for longer than anticipated, it could exert further downward pressure on property valuations and make debt refinancing more expensive, impacting profitability.

Concentration Risk: Around 75% of SUPR’s rental income is derived from Tesco and Sainsbury's, which presents tenant concentration risks. Any financial distress or strategic shifts by these tenants could significantly impact the REIT’s cash flows. The UK retail market has shown vulnerabilities, and although grocery retail is defensive, the broader economic pressure could still affect consumer spending.

Foreign Exchange and Integration Risks: The recent expansion into France with Carrefour stores introduces currency and integration risks. While this diversification can provide growth opportunities, it also exposes the company to fluctuations in the Euro and potential operational integration challenges.

Market Sentiment Towards REITs: Investor sentiment towards real estate, particularly REITs, has been lukewarm due to concerns over interest rates and property market dynamics. This has resulted in a subdued stock price performance, with SUPR trading near its 52-week low. Sustained market scepticism could limit capital appreciation potential

Conclusion

Supermarket Income REIT appears well-positioned for long-term investors seeking income stability with an 8.47% dividend (as of Oct 23rd 2024) from a defensive asset class, with potential for growth driven by strategic acquisitions and the continued resilience of grocery retail. However, risks related to interest rates, tenant concentration, and broader market sentiment must be carefully considered. A balanced approach would involve assessing the stock's valuation relative to the risk-reward profile, particularly in the context of interest rate outlooks.

Click graphic to expand trade plan

_________________________________________________________

Warpaint London - Strong growth and increasing dividend - We're made up! - Sept 20th 2024

AOA currently holds W7L

Warpaint London PLC (LSE:W7L) - Warpaint London PLC sells branded cosmetics under the brand names, W7 and Technic. The reportable segments of the company are Own Brand and Closeout. The branded sales relate to the sale of own branded products whereas 'close-out' relates to the purchase of third-party stock which is then repackaged for sale. The company generates a majority of its revenue from its Own brand segment. Geographically, the company derives maximum revenue from the UK and operates in Europe, the USA, Australia, New Zealand, and the Rest of the World.

Shares climbed 8% on latest results (Sep 2024) after it increased first-half profits more than expected, as the cosmetics group focused on increasing sales of its W7 and Technic brands around the world.

Revenues of £45.8 million were generated in the first six months of 2024, up 25%, with operating profits leaping 75% to £11 million.

UK revenue increased 17% to £15.5 million and international revenue by 30% to £30.3 million.

Gross profit margin increased to 42.5% from 39.1% a year ago, which the company put down to the launches of new product lines, savings from sourcing and volume savings, more e-commerce revenue and increased US profitability.

With cash of £6.5 million as of 1 July, the board declared an increased interim dividend of 3.5p per share, up 17%.

Chief executive Sam Bazini said the growth in sales and profits reflected "the ongoing success of the group's strategy of focusing on growing profitable sales of its branded products globally, whilst increasing overall margins". He added: "There continues to be significant growth opportunities for Warpaint, and the group is very well positioned to achieve further growth with additional improvement in margins." Sales are expected to be weighted to the second half, reflecting Christmas seasonal sales and ongoing sales momentum, Bazini said. - Source RNS & Proactive

At AOA we believe the US market potential (10x UK market) provides major revenue growth and also see this company as a potential bid opportunity as the founders near retirement.

Click graphic to expand trade plan

_________________________________________________________

Oxford Metrics - A Hidden Gem - Sept 6th 2024

AOA does not currently hold OMG

Oxford Metrics (AIM:OMG) Oxford Metrics (OMG) is a hidden gem in the UK technology sector a global leader in motion capture technology. https://oxfordmetrics.com/about

Oxford Metrics PLC develops and markets analytics software for motion measurement and infrastructure asset management. The company comprises one business segment: The Vicon Group is engaged in the development, production, and sale of computer software and equipment for the engineering, entertainment, and life science markets. The firm operates in United States and United Kingdom : MCAP £112m, Share Price 85.6p (Aug 20th 2024), 1yr Price target £1.47

Interim Results 23/24- https://oxfordmetrics.com/videos

2024 Capital Markets Day - https://www.youtube.com/watch?v=wClUZsCbAqk

Why Oxford Metrics Stands Out

Market Leadership: Vicon is a dominant player in motion capture, a technology essential for industries ranging from entertainment (think blockbuster movies and video games) to healthcare and engineering. As demand for immersive experiences and precise data analysis grows, Vicon is well-positioned to capitalize on these trends.

Financial Health: Oxford Metrics boasts a strong balance sheet with no debt, providing a solid foundation for future growth. The company’s consistent revenue generation, particularly from high-margin services, contributes to its financial stability. - https://oxfordmetrics.com/financials

Strategic Innovation: The company’s focus on R&D and its foray into AI and machine learning suggest a commitment to staying ahead in the tech space. This strategic vision is key to maintaining its competitive edge in a rapidly evolving market. - https://oxfordmetrics.com/strategy

Diversification: With Vicon serving global markets, OMG is diversifying across different market segments through M&A - https://oxfordmetrics.com/news/2023-11-01/acquisition-of-industrial-vision-systems-ltd-and-issue-of-equity

Key Risks to Consider

Market Cyclicality: Vicon’s reliance on the entertainment and sports sectors makes it vulnerable to economic downturns, which could reduce demand for its technology.

Technological Disruption: The tech landscape is ever-changing. Oxford Metrics must continue to innovate to fend off potential competitors offering more advanced or cost-effective solutions.

Customer Concentration: A significant portion of Vicon’s revenue comes from a few large clients. Losing any of these clients could have a substantial impact on the company’s financials.

Economic and Regulatory Risks: Like any global company, Oxford Metrics is exposed to economic fluctuations and potential changes in regulations that could impact its operations.

Currency Fluctuations: With revenue streams from multiple regions, the company is subject to the whims of currency exchange rates, which could affect its profitability.

Oxford Metrics offers a compelling investment opportunity in the tech sector, particularly for those looking to gain exposure to the growing fields of motion capture and smart sensing. However, potential investors should weigh the company’s innovative strengths and market leadership against the inherent risks in its operations and industry. With careful consideration, Oxford Metrics could be a valuable addition to a diversified portfolio.- https://oxfordmetrics.com/news/2024-04-25/capital-markets-day-2024

Source : SharePad

Yu Group - Results in line with expectations yet stock drops >25%. We think that's overdone - July 25th 2024

AOA does not currently hold YU.

Yu Group PLC (LSE: YU) on Tuesday July 22nd announced strong growth in revenue in the first half of 2024.

Yu is an Nottingham, England-based independent supplier of gas and electricity, meter asset owner, and installer of smart meters to the UK corporate sector.

Yu said revenue increased by 60% to approximately GBP310 million in the six months that ended June 30 from GBP195 million a year before, despite "mild spring temperatures" in the UK.

Monthly average bookings declined by 8.6% to GBP46.9 million in recent six months from GBP51.3 million a year before. Yu said this reflected lower commodity market prices.

More positively, Yu delivered a 35% increase in supplied meter points and an 125% increase in meter installations in the first half of the year.

Yu noted it implemented a five-year commodity hedging agreement with Shell Energy, part of Shell PLC, during the recent half, positioning the group for "significant scale", said Chief Executive Officer Bobby Kalar.

Looking forward, Yu expects to deliver earnings before interest, tax, depreciation and amortisation and an Ebit margin in line with market expectations for 2024.

Kalar said: "I remain excited by the future and am fully committed to delivering shareholder value."

Yu will release results for the half-year on September 24. - Source - Alliance News

Shares in Yu were down 25% to ~1400 pence each in London on Thursday. AOA think this is an overdone reaction to the recent results and have taken a position at this price level on July 25th.

Softcat - Is the recent downgrade from Jefferies a little too harsh for this £3.6Bn IT company? -July 9th 2024

AOA currently holds SCT

AOA are currently looking at SOFTCAT for a short term 15-20% swing trade through the summer

Analysts at Jefferies downgraded IT infrastructure provider Softcat to 'underperform' on Friday, citing "incremental caution" around the IT services sector. So far in July the stock has lost almost 12% over the first several trading days in July.

Jefferies thinks FY24 consensus estimates for Softcat look "reasonable" but noted that FY25-26 consensus of 12-13% underlying earnings growth was already ahead of the company's typical framework to target low double-digit gross profit growth and high single-digit EBIT growth.

"We think this puts downward pressure on consensus," said Jefferies.

The investment bank also noted that Softcat trades on one of the highest valuations in European tech, with valuations that were more consistent with roughly 20-25% EBIT growth.

"Given the forecast risk, this premium valuation looks exposed," said Jefferies. "We align DCF assumptions with the same metrics used at Bytes, leading us to downgrade our price target to 1,490.0p and move our rating to 'underperform'." source - Sharecast

We don't agree with Jefferies on the comparison with Bytes (the latter having had all sorts of management issues - see below) and wonder if this is another 'positioning' downgrade. Financials still strong with FCF of £103m and minimal debt of ~£10m.

Support is at around £15 (-17% from start of July) which is our next area of interest for this trade.

'Ole Ole Ole Ole' - Which Stocks may benefit from the Euro 2024 football tournament?

AOA does not currently hold any of these stocks

AOA took a position in Domino’s (LSE:DOM) yesterday at £3.15 on the back of a prospective uptick due to Euro 2024 football and the propensity of people ordering takeaway for the matches. This one usually gets a seasonal boost as more people order food while watching the football.

Other UK stocks likely to benefit from the Euro 2024 football festival span various sectors, primarily those related to travel, consumer goods, retail, and media. Here are some key stocks to watch with todays (Jun 13th) prices added.. lets see.

1. International Consolidated Airlines Group (LSE:IAG): As the parent company of British Airways and other airlines, IAG is poised to benefit from increased travel demand during Euro 2024. The tournament will drive higher passenger volumes, boosting revenues from flights to and from the event locations in Germany. £1.67

2. ITV (LSE: ITV): As a major broadcaster, ITV stands to gain from advertising revenues linked to Euro 2024. The event will likely attract significant viewership, providing a lucrative platform for advertisers. £0.77

3. JD Sports Fashion (LSE: JD.): With the increased interest in sports and related merchandise during Euro 2024, JD Sports is expected to see a rise in sales of sportswear and football-related products. £1.22

4. Marks & Spencer Group (LSE: MKS): As a prominent retailer, Marks & Spencer could benefit from higher sales of food, beverages, and other consumer goods as fans host and attend viewing parties. £2.99

5.Currys (LSE:CURY): New TV for a better viewing experience? - Electronics retailers should benefit from increased sales £0.77

What other companies do you think will benefit from the football mania?

Raspberry Pi - Good value at £2.80 a share or will it suffer from lack of UK Interest in the months ahead ? - June 11th 2024

AOA currently holds this stock

Computer-maker Raspberry Pi is set to raise £157m in a boon for the London Stock Exchange after a barren period for tech listings. The Cambridge-based tech outfit is set to raise $40m (£31.5m) in fresh funding via the float while its largest shareholder, the Raspberry Pi Foundation, will offload a chunk of its share to investors. Shares are to be priced at £2.80 through June 10, with conditional trading starting on June 11. Under the terms of the deal, about 20 per cent of Raspberry Pi’s shares will be traded freely on the market. Some £6.8m worth of shares will also be earmarked for retail investors. - source Yahoo Finance

Expected timetable of principal events

Event Time and Date Prospectus published / Announcement of Offer Price and notification of allocations of Offer Shares in the Global Offer 1 June 2024

Commencement of conditional dealings on the London Stock Exchange 8.00 a.m. on 11 June 2024

Admission and commencement of unconditional dealings on the London Stock Exchange 8.00 a.m. on 14 June 2024

CREST accounts credited in respect of Offer Shares acquired in the Global Offer in uncertificated form 14 June 2024

Despatch of definitive share certificates (where applicable) From 14 June 2024 and within ten Business Days of AdmissionMore info on the June 11th 2024 IPO can be found at https://investors.raspberrypi.com/ipo

Update (June 13th) - ~£800m Valuation at £4.11 a share. That looks overbaked considering annual revenues of ~£30m.... We fully expect a drop in price in the days to come once general retail have bought their slice.

Diageo (LSE:DGE) Anyone fancy a tipple at these prices ? - May 30th 2024

AOA does not hold this stock

Diageo (DGE) is approaching an interesting price zone for a possible turnaround level based on where previous buyers got interested in October 2020. Here's what AoA are looking at and waiting patiently for an entry around £25. A dividend at around 3.6% is available at that level and a decent risk reward.

Bytes Technology Group (LSE:BYIT) - CEO leaves and stock drops 14% - A Buying Opportunity ?

Feb 23rd 2024: What's the CEO doing buying and selling stock without informing the board?

Neil Murphy resigned this week with immediate effect after informing the board that he had been buying an selling stock in the company without disclosing it formally. The stock fell 14% on the news.

Here's some further detail from the following RNS - https://www.londonstockexchange.com/news-article/BYIT/director-pdmr-transactions-late-notification/16345732

Further to the announcement made on 21 February 2024 regarding the resignation of the Company's CEO, Neil Murphy, the Board has been notified of the below trades made by Neil Murphy since the Company's IPO on 11 December 2020 which have not been previously notified or otherwise disclosed to the Company as required by Article 19 of the Market Abuse Regulation (EU) 596/2014 of 16 April 2014, which is part of UK law by virtue of the European Union (Withdrawal) Act 2018 ("MAR").

As noted in the earlier announcement, the Company understands that Neil Murphy's current holding of BTG's shares is 2,890,218 and remains unchanged from the position notified to the market on 28 November 2023. In aggregate, the below trades total to 313,741 shares acquired at a volume weighted average price of 479.23 pence per share and 313,741 shares sold at a volume weighted average price of 483.46 pence per share.

Now the question is simply, why? With 2.8m shares already it wasn't like he had any need to do this. Either way he's gone and Sam Mudd (Board member of BTG and MD of Phoenix Software Ltd) has taken the role of Interim CEO.

Having reviewed the latest results, (https://www.bytesplc.com/application/files/4816/9822/1112/BTG_interim_results_31_Aug_23.pdf) the company looks in good shape and is growing with revenues improving by 16.3% to come in at £108.7m with a climb of 13.8% in adjusted operating profit to £33.9m. During the period, the firm managed to secure some sizeable public sector deals as well as keep enterprise demand ticking over. Other highlights included increasing headcount by almost 10% and keeping a solid customer base with renewal rates of 113%.

Bytes is positively dripping in certifications, and remains one of the few local solution providers to have all six Microsoft designations for business applications, data & AI, distal and app innovation, infrastructure, security and modern workplace. We think this represents a buying opportunity while management sort themselves out.

AOA does not currently hold this stock

Jan 24th 2024: - Looking at Netcall this morning after yesterdays results. Netcall PLC is a United Kingdom-based company engaged in the design, development, sale and support of software products and service The company has only one operating business segment being the design, development, sale and support of software products and services. The company derives revenue from Product support contracts; Cloud services; Communication services, Product and Services. majority revenue is generated from Cloud services.

Although 'in line' I like the recurring revenue streams and the fact that it's debt free. - https://www.netcall.com

MCAP: £152m

Share Price growth over the last three years was

2021 36.6%

2022 41.3%

2023 -7.7%

2024 ytd 2.8%

Price now above 200 SMA and ~90p looks like a good entry level for a possible break. Target 1 (T1) £1.16 or ~30% above entry. T2 £1.30.

From yesterdays TU: https://www.londonstockexchange.com/news-article/NET/trading-update-and-notice-of-results/16299457

The Board is pleased to confirm that the Group experienced good trading in H1 FY24 with results expected to be in line with management expectations. Revenue is anticipated to increase by 8% to £18.9m (H1 FY23: £17.5m) with adjusted EBITDA(1) growth of 9% to £4.8m (H1 FY23: £4.4m).

Cloud annual contract value ('ACV')(2) has grown 19% to £20.3m, contributing to total ACV growth of 14% to £30.1m. On an underlying basis, these growth rates are 28% and 18% respectively, excluding the effect of the significant contract win announced in June 2022 and renewed in July 2023.

In order to service a growing pipeline and deliver an improved proposition, the Group's investment programme into its cloud Customer Engagement offering has commenced as planned.

The Group generated strong cash flow in the period, resulting in a period end cash position of £28.6m (30 June 2023: £24.8m). The Group has no debt.

AoA does not currently holds this stock.

----

Netcall (LSE:NET) - A growth story or possible bid target for 2024?

BOKU (LSE:BOKU) - A Cash Generating Machine?

Jan 24th 2024: - Looking at BOKU Inc a carrier billing company. It's technology enables mobile phone users to buy goods and services and make online payments using their mobile devices. The company's operating segment includes Payments and Identity. It generates maximum revenue from the Payments segment, which is engaged in the provision of a payment platform that enables mobile phone users to buy goods and services and charge them to their mobile phone or prepaid balance. Spiked up yesterday after a strong trading update. - https://www.boku.com

MCAP: £490m, Total company shares 297.1m

Share Price growth over the last three years was

2021 13.1%

2022 -15.2%

2023 -4.3%

2024 ytd 23.6%

Price now above 200 SMA and ~160p looks like a good entry level on a breakout pullback. Target 1 (T1) £2.12 or ~31% above entry.

Financial Highlights from trading update 23rd Jan 2024.

Revenues for the year ended 31 December 2023 are expected to be at least $82.7m (2022: $63.8m), up 30% andup 33% on a constant currency basis**** driven by increasing transaction volumes from our major global merchants including good growth from bundling.

H2 2023 revenues expected to be at least $44.5m representing 33% growth compared to H2 2022 (H2 2022: $33.4m).

Full year revenues include $16.9m from Local Payment Methods ("LPMs"), up 153% from $6.7m in 2022 following increasing adoption of these products by our key merchants.

Adjusted EBITDA* expected to be at least $27.3m, up 33% from $20.5m in 2022, and ahead of current market expectations, despite continued investment in Boku's mobile-first payment network with adjusted EBITDA margin of approximately 33%.

Total Group cash was $151.2m at year-end, up from $113.9mat 30 June 2023 and $116.3m at 31 December 2022. Of this, approximately $69.0m is Boku's 'own cash' with the balance being merchant cash in transit. The Group has no debt.

Full info on the latest TU - https://www.londonstockexchange.com/news-article/BOKU/trading-update/16299477

AoA does not currently hold this stock.

Please Note: Any information or opinions provided should not be considered as tips or financial advice. Investing in stocks or any other financial instruments involves inherent risks, and decisions made based on the information provided are solely your responsibility. Please always remember to conduct your own research before making any investment decisions. Please refer to Terms and Conditions for more details.